Summary

- Case Overview: The UK Court of Appeal’s judgment in R v Andrew Lakeman (2026) establishes that virtual in-game currency, specifically RuneScape gold pieces, constitutes “property” under English criminal law, impacting how such digital assets may be treated in indirect tax contexts. Although the case does not address VAT directly, it signals potential implications for the valuation and categorization of digital assets in future tax assessments.

- Court Decision: The Court overturned a lower court’s dismissal of theft charges, emphasizing that in-game currency is not just “pure information” and possesses identifiable, exclusive characteristics with economic value. The judgment clarifies that the concept of property in criminal law can extend to digital assets, rejecting the notion that infinite supply negates their rivalrous nature, similar to fungible items like money.

- Implications for VAT and Indirect Tax: The recognition of in-game currency as property may influence how such assets are treated for VAT purposes, suggesting they can be supplied, valued, and exchanged in economically real transactions. This shift towards acknowledging the economic substance of digital assets could pave the way for future VAT considerations in virtual economies, despite the current absence of direct VAT rulings in the case.

Detailed

- Introduction

R v Andrew Lakeman is a 2026 judgment of the UK Court of Appeal (Criminal Division) that has attracted significant attention across legal, gaming, and digital‑asset communities. Although the case does not concern VAT directly, it is highly relevant for indirect tax specialists because it establishes that virtual in‑game currency can constitute “property” under English criminal law.

This recognition has potential downstream implications for VAT characterisation, valuation, supply analysis, and enforcement in virtual economies. The decision marks a major step in the UK courts’ engagement with economically valuable digital assets beyond traditional cryptoassets. [iclr.co.uk], [cms-lawnow.com]

- Factual Background

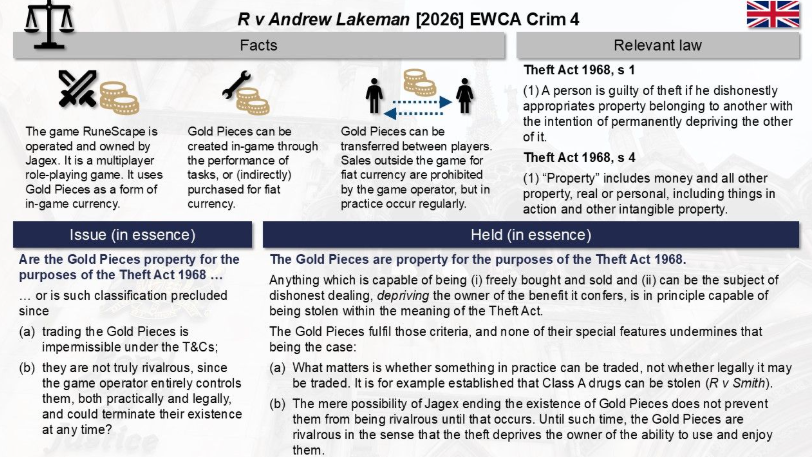

Andrew Lakeman was employed as a content developer by Jagex Ltd, the UK company behind the online game Old School RuneScape. Prosecutors alleged that between 2018 and 2019, he unlawfully accessed 68 player accounts by hacking or misusing internal credentials and transferred approximately 705 billion “gold pieces” (the game’s in‑game currency) out of those accounts.

The stolen gold was then allegedly sold outside the game for Bitcoin and fiat currency, generating proceeds estimated at £543,123. [casemine.com], [cms-lawnow.com]

Lakeman was charged with:

- Unauthorised access to computer material (Computer Misuse Act 1990),

- Theft under section 1 of the Theft Act 1968, and

- Money laundering offences under the Proceeds of Crime Act 2002.

The theft count became the pivotal issue. [casemine.com]

- The Legal Issue Before the Court

At a preparatory hearing, the Crown Court judge dismissed the theft count, holding that RuneScape gold pieces were not “property” within section 4 of the Theft Act 1968.

The judge accepted the defence argument that the gold was:

- “Pure information”, and

- Non‑rivalrous, because the overall supply of gold in the game is theoretically unlimited.

The prosecution appealed this ruling to the Court of Appeal. [casemine.com]

- Decision of the Court of Appeal

4.1 Gold Pieces Are “Property” Under the Theft Act

In a judgment delivered on 14 January 2026, the Court of Appeal (Popplewell LJ, Soole J and Mayo HHJ) allowed the prosecution’s appeal, holding that RuneScape gold pieces are “property” capable of being stolen. [iclr.co.uk]

The Court emphasised that:

- The Theft Act adopts a criminal‑law concept of property, not a civil‑law one.

- Items may be property even if civil ownership rights are limited or contractually constrained.

- The correct question is whether the item is something that can sensibly be described as stolen. [casemine.com]

4.2 Rejection of the “Pure Information” Argument

The Court distinguished in‑game gold from “pure information” (as in Oxford v Moss), noting that gold pieces:

- Exist as identifiable, discrete digital assets on Jagex’s servers,

- Are exclusive in use (only one player can control specific units at a time),

- Are functional assets within the game economy, not mere knowledge. [casemine.com]

4.3 Rivalrousness and Economic Reality

The Court rejected the argument that infinite supply defeats rivalrousness, comparing gold pieces to paper clips or money—fungible, infinitely producible, yet still property.

Crucially, the Court noted that gold pieces have:

- Ascertainable monetary value, and

- A real‑world exchange market, even if prohibited by the game’s terms of service. [ign.com], [thisweekin…ogames.com]

- What the Case Is Not About: VAT

It is important to be clear:

❌ R v Lakeman does not decide any VAT issues

❌ No supplies, consideration, place of supply, or exemptions were analysed

❌ HMRC was not a party, and VAT legislation was not considered

The case is purely criminal law, focused on the definition of “property” for theft. [iclr.co.uk]

- Why the Case Matters for VAT and Indirect Tax

Despite the absence of a VAT ruling, R v Lakeman is highly relevant for VAT practitioners, particularly those dealing with digital platforms, gaming, and virtual economies.

6.1 Recognition of Virtual Currency as an Asset

The Court’s acknowledgment that in‑game currency is:

- Identifiable,

- Exclusive,

- Economically valuable,

supports the argument that such assets may constitute “something” capable of being supplied for VAT purposes, depending on the structure of transactions. [cms-lawnow.com], [lexology.com]

6.2 Implications for Taxable Supplies

Where in‑game currency is:

- Sold for fiat currency,

- Exchanged for cryptoassets,

- Bundled with digital services (e.g. game time, upgrades),

the Lakeman reasoning strengthens the view that these are economically real transactions, not merely internal accounting entries. [lexology.com]

6.3 Valuation and Consideration

The Court accepted evidence of:

- External market value,

- Conversion into money’s worth,

which aligns with VAT concepts of consideration expressed in monetary terms, even where transactions occur in non‑traditional markets. [cms-lawnow.com]

- Broader Significance

R v Lakeman represents:

- The first English appellate authority confirming that virtual in‑game currency can be stolen,

- A judicial shift toward economic substance over digital form, and

- A foundation for future cases involving digital assets, NFTs, virtual worlds, and metaverse economies. [brownejacobson.com]

While VAT law will require separate statutory and EU‑derived analysis, Lakeman removes a key conceptual barrier: the idea that virtual assets are legally “nothing”.

- Conclusion

R v Andrew Lakeman [2026] EWCA Crim 4 is not a VAT case, but it is a critical building block for future VAT analysis of digital and virtual assets. By recognising in‑game currency as “property” with real economic value, the Court of Appeal has aligned criminal law with commercial reality—an approach that VAT law, which is fundamentally transaction‑ and value‑driven, is likely to follow.

For VAT specialists advising on gaming, digital platforms, and virtual economies, Lakeman is now essential reading.

Latest Posts in "United Kingdom"

- HMRC Confirms VAT Exemption for Locum Doctors After Landmark Isle of Wight NHS Tribunal Decision

- VAT Rates: 5% for Renewable Energy Installations, 20% for Double Glazing

- Company Liable for Unpaid Import VAT Due to EORI Confusion and Lack of Evidence, Appeal Dismissed

- VAT Input Tax Denied for Nursery Property: Option to Tax Disapplied in Nissi N Nissi Ltd Case

- HMRC Introduces Mandatory Registration for Tax Advisers from May 2026: Key Rules and Exemptions