Key takeaways

- Voucher treatment requires real discipline in design. The UT draws a sharp distinction between a VAT “voucher” and the sale of an already effective right to receive services. To rely on voucher rules, businesses must clearly create and define a genuine instrument and its redemption conditions; prepaid access or availability alone will not suffice.

- Economic reality prevails over form. Where customers are effectively purchasing time‑limited access or availability of services, VAT arises at the point of sale, regardless of whether or how the services are later used. The case highlights how unstable, in practice, the conceptual boundary can be between a right to use a service and a right to redeem a voucher.

- Use & enjoyment overrides survive single‑supply analysis. The UT confirms that use and enjoyment place‑of‑supply rules are not neutralised by characterising arrangements as a single (or composite) supply. While the specific rule applied in this case has since fallen away, the principle remains relevant wherever such overrides continue to apply.

Other source

Detailed

Lycamobile: Upper Tribunal Clarifies the VAT Boundary Between Vouchers, Prepaid Rights and Use & Enjoyment

Overview

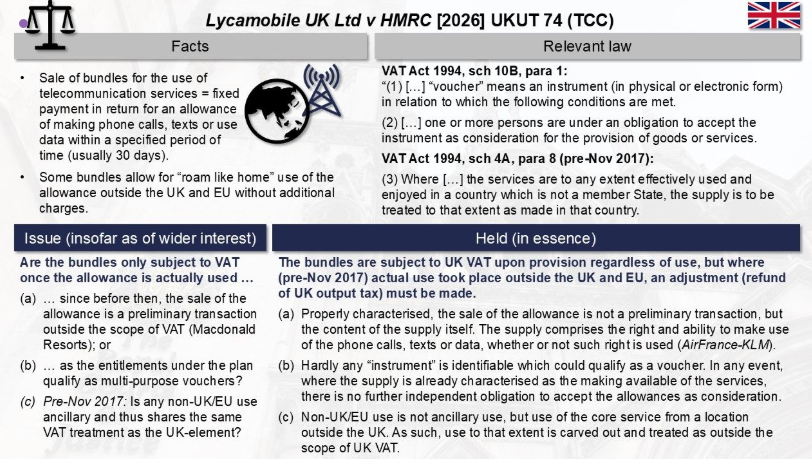

In Lycamobile UK Ltd v HMRC [2026] UKUT 74 (TCC), the UK Upper Tribunal (UT) has delivered an important decision on the VAT treatment of prepaid telecoms bundles, rejecting arguments that VAT should arise only when services are actually consumed or that the arrangements fell within the VAT voucher regimes. Instead, the UT confirmed that VAT was chargeable in full at the point of sale of the bundles, reflecting the economic reality that customers were purchasing time‑limited access to telecom services rather than a mere instrument to be redeemed later. The decision also provides valuable clarification on the interaction between the single (or composite) supply doctrine and use and enjoyment place‑of‑supply overrides. [gov.uk], [11newsquare.com]

The case has significance well beyond telecoms, particularly for businesses operating prepaid, subscription‑based, or hybrid models across borders.

Background to the dispute

Lycamobile UK Ltd (LMUK), a mobile virtual network operator, sold various prepaid “plan bundles” to UK customers. Each bundle entitled the customer, for a fixed validity period (typically 7, 14 or 30 days), to specified allowances of calls, texts and/or data. Some bundles also included access to value‑added services (VAS) or the ability to use allowances while roaming outside the UK. Unused allowances expired at the end of the validity period. [assets.pub…ice.gov.uk], [casemine.com]

LMUK accounted for VAT only when, and to the extent that, allowances were actually used, on the basis that the relevant supply occurred when telecom services were consumed. HMRC disagreed and assessed VAT on the full consideration received at the point of sale or activation of the bundles, issuing assessments exceeding £50 million for periods between 2017 and 2019. [assets.pub…ice.gov.uk], [vatfaqs.com]

The First‑tier Tribunal (FTT) largely upheld HMRC’s position. LMUK appealed to the Upper Tribunal, advancing four main grounds, including arguments that the bundles represented rights to future supplies only, and that they constituted vouchers for VAT purposes. HMRC cross‑appealed on aspects of the FTT’s treatment of non‑EU usage. [claritaxnews.com], [11newsquare.com]

Timing of the supply: access versus use

At the heart of the case was a familiar VAT question: when is the taxable supply made? LMUK argued that the “real” supply occurred only when customers actually made calls, sent texts or used data, and that VAT could not arise earlier because the precise nature and place of supply were not yet known. [assets.pub…ice.gov.uk], [11newsquare.com]

The UT rejected this analysis. It agreed with the FTT that, viewed objectively, the supply made by LMUK was the grant of access or availability to specified telecom services for a defined period. That supply was complete, and reciprocal obligations existed, at the point when the bundle was sold or activated. Actual use of allowances was merely the exercise of a right already supplied, not a separate taxable event. [11newsquare.com], [claritaxnews.com]

In reaching this conclusion, the UT drew analogies with other familiar business models, such as gym memberships or streaming subscriptions, where VAT is due on the price paid for availability or access, irrespective of whether the customer ultimately makes full use of the service. The fact that some allowances might never be used did not prevent the existence of a taxable supply at the outset. [11newsquare.com], [accountingweb.co.uk]

Why the bundles were not VAT “vouchers”

As an alternative argument, LMUK contended that the plan bundles should be treated as vouchers under the UK’s VAT voucher regimes (Schedules 10A and 10B VATA), such that VAT would arise only on redemption, i.e. when allowances were used. [claritaxnews.com], [11newsquare.com]

The UT firmly rejected this position. It endorsed the FTT’s conclusion that the arrangements lacked the essential characteristics of a voucher. In particular, customers were not acquiring a separate instrument whose sole function was to be exchanged for supplies at a later point. Instead, they were purchasing a package of defined entitlements that took effect immediately upon activation. The “real subject” of the transaction was the bundle itself, not a voucher standing in for later supplies. [11newsquare.com], [simmons-simmons.com]

The decision underscores a critical practical point: voucher treatment cannot be achieved by labelling alone. If businesses wish to rely on the VAT voucher rules, they must ensure that they genuinely create and define an identifiable instrument, with clear redemption conditions and a meaningful distinction between the issue of the instrument and the supply of the underlying services. Where the economic reality is that the customer is buying present access or availability, the voucher rules are unlikely to apply. [11newsquare.com], [claritaxnews.com]

An unstable boundary: right to use vs right to redeem

The UT’s reasoning also highlights a broader structural tension in VAT. There is a fine but important line between:

- a right to use a service over time (treated as a present supply of services), and

- a right to redeem an instrument for future supplies (potentially falling within the voucher regimes).

In modern prepaid and digital business models, that distinction can become conceptually unstable. Lycamobile demonstrates that courts will look past form and focus on economic substance, particularly on whether the customer has already obtained something of value at the point of payment, even if later consumption is uncertain. [11newsquare.com], [assets.pub…ice.gov.uk]

Use & enjoyment and the limits of single‑supply analysis

A further important aspect of the decision concerns use and enjoyment place‑of‑supply rules. HMRC cross‑appealed aspects of the FTT decision that had allowed adjustments for certain non‑EU usage, arguing that once the bundles were characterised as a single (or composite) supply, it was inappropriate to revisit where elements of that supply were used or enjoyed. [11newsquare.com], [accountingweb.co.uk]

The UT rejected HMRC’s cross‑appeal. It confirmed that use and enjoyment overrides operate independently of the single‑supply doctrine. While supply characterisation determines what is supplied, statutory use and enjoyment provisions (where applicable) can still adjust the place of supply by reference to where services are actually used or enjoyed. This approach is consistent with EU case law and established VAT principles. [11newsquare.com], [assets.pub…ice.gov.uk]

Although the specific use and enjoyment provision relevant to part of the dispute is no longer in force in the same form, the UT’s reasoning remains highly relevant for other use and enjoyment rules that continue to apply. Businesses cannot assume that a single‑supply analysis will neutralise such overrides. [11newsquare.com], [claritaxnews.com]

Practical implications for businesses

The Lycamobile decision carries several practical lessons:

- Prepaid and subscription models should expect VAT to arise at the point of sale where customers acquire time‑limited access or availability, even if actual usage is low or uncertain.

- Voucher strategies must be carefully designed. To benefit from voucher rules, businesses need a genuine instrument with clearly defined redemption mechanics, not merely prepaid access branded as “credit”.

- Cross‑border services must still be tested against use and enjoyment overrides, even where supplies are characterised as single or composite.

These points are relevant not only to telecoms operators, but also to digital platforms, travel and leisure providers, and any business offering prepaid or bundled access to services across jurisdictions.

Conclusion

The Upper Tribunal’s decision in Lycamobile reinforces a substance‑over‑form approach to VAT in prepaid and access‑based business models. It clarifies the limits of voucher arguments, confirms the primacy of economic reality in determining the timing of supplies, and reaffirms that use and enjoyment overrides are not displaced by single‑supply analysis. For businesses operating in this space, the case is a timely reminder that VAT outcomes must be tested carefully against both commercial design and statutory structure. [gov.uk], [11newsquare.com]

VAT Treatment of Consideration Received by Lycamobile UK Ltd: Court Decision on Telecommunication Service Bundles

- The Upper Tribunal ruled that Lycamobile’s bundled telecommunication services are subject to VAT at the point of sale, not as the services are used, leading to the taxpayer being liable for the full VAT amount upfront rather than deferring it based on service usage.

- The bundles were determined not to qualify as vouchers under both pre-2019 and post-2019 UK VAT rules, as they did not meet the statutory definition required for vouchers, which would allow different VAT treatment.

- The court confirmed that while retrospective adjustments for VAT are required for services used outside the EU before November 2017, the full VAT is due at the time of sale for services used within the UK or EU, resulting in a potential liability of approximately £51 million for the taxpayer.

Source KPMG

Latest Posts in "United Kingdom"

- UK Care Provider Liable for VAT Under Reverse Charge on Slovak Staff Supply, Tribunal Rules

- FTT: Input VAT Recoverable Despite Minor Invoice Defects; HMRC Must Exercise Discretion Reasonably

- FTT Rules Personalised Biography Books Zero-Rated for VAT Despite Ghost-Writing Services Involved

- Severe Female Hair Loss Deemed Disability for VAT Zero-Rating of Hair Replacement Services

- Splend SPV (UK) Ltd Appeal Against VAT Late Payment Penalties Dismissed by FTT