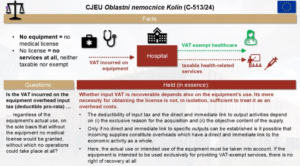

- Dispute over Input VAT for Partially Exempt Hospital: Oblastní nemocnice Kolín, a Czech hospital offering both exempt healthcare and taxable additional services, claimed input VAT on overheads. Tax authorities challenged part of the claim, arguing it related to non-deductible healthcare services, leading to a reference to the ECJ on the proportional deduction of VAT under Article 173(1).

- Legal Obligation Alone Does Not Justify VAT Deductibility: The Court ruled that a mere legal obligation to make a purchase does not automatically justify VAT deductibility. Instead, deduction depends on a factual, objective assessment of how each purchased item is actually used within the taxable person’s economic activities.

- No Proportional Deduction for Healthcare Service Costs: The ECJ concluded that non-deductible costs directly related to healthcare services do not constitute general overheads with a direct and immediate link to the taxable person’s overall economic activity. Therefore, these specific costs do not give rise to a right to proportional VAT deduction.

Source KPMG

- Oblastní nemocnice Kolín, a hospital, provides both VAT-exempt health services (requiring minimum equipment for licensing) and VAT-deductible services, leading to a dispute over VAT deduction on equipment purchases.

- The hospital argued for VAT deduction on goods and services forming part of the legally required minimum equipment, even if primarily used for VAT-exempt health services.

- The Court of Justice ruled that the legal requirement for minimal equipment is not enough to establish a direct and immediate link to VAT-deductible output transactions; only the objective relationship between input and output transactions is decisive for VAT deduction.

Source Taxlive

See also

ECJ Rules on VAT Deduction for Legally Mandated Equipment

- The European Court of Justice (ECJ) ruled that a Czech hospital, Oblastní nemocnice Kolín, cannot claim a proportional VAT deduction on equipment primarily used for VAT-exempt health services, even if legally mandated.

- The hospital argued that this equipment was necessary to obtain the authorization to provide all services, including VAT-deductible ones, therefore qualifying as general costs for its overall economic activity.

- The ECJ clarified that a legal obligation alone is not enough to establish a direct link to a taxable person’s overall economic activity for VAT deduction; the actual use and objective relationship of the goods/services are the decisive factors.

Source BTW Jurisprudentie

- Linking input VAT to output transactions is complex, requiring a “direct and immediate link” where the actual use of goods or services often outweighs other factors, even legal obligations.

- The recent ECJ ruling on Oblastní nemocnice Kolín confirms this: equipment purchased due to a legal requirement for exempt services does not automatically qualify for proportional VAT deduction as a general cost if its primary use is for those exempt services.

- This judgment aligns with previous rulings, emphasizing that the objective relationship and intended use, rather than just the obligation to acquire, are the decisive elements for VAT deductibility, similar to how UK courts have treated “interdependent business activities.”

Source Fabian Barth

- See also

- Join the Linkedin Group on Global E-Invoicing/E-Reporting/SAF-T Developments, click HERE

- Join the LinkedIn Group on ”VAT in the Digital Age” (VIDA), click HERE

Latest Posts in "European Union"

- EGC Customs T-296/25 (Lidikar) – Judgment – Use of Foreign Export Prices for EU Customs Valuation

- Comments on ECG T-689/24: Confirms Incompatibility of Polish Input VAT Deduction Rules with EU Law

- Comments on T-221/25: Implicit VAT taxation for non-EU travel services by agents is valid

- ECJ/General Court VAT Cases – Pending cases

- ECJ & General Court VAT Cases decided in 2026