Triangular Transactions in Focus: General Court Rejects German Tax Authority’s View

- The General Court ruled that triangular transaction simplifications can apply to chain transactions involving more than three parties, emphasizing that physical possession of goods is not required, but rather the legal ability to dispose of the goods is key.

- The court’s decision challenges the restrictive interpretation of the German tax authority, which had previously denied triangular transaction simplifications if the last three parties in the chain were not involved, leading to significant tax and administrative burdens for taxable persons.

- The ruling stresses that the simplification does not apply if a taxable person is aware or should be aware of VAT fraud within the supply chain, reinforcing the need for due diligence and accurate documentation to ensure compliance and mitigate potential tax liabilities.

Source KMLZ

ABC regulation in four-party chain: physical delivery and abuse

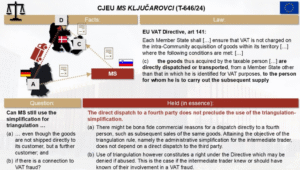

- Triangular Transaction and VAT Fraud: The Slovenian intermediary MS KLJUČAROVCI engaged in a triangular transaction scheme by purchasing goods from German suppliers and selling them to Danish customers, while the goods were actually transported directly to a fourth party in Denmark. The Slovenian tax authorities deemed this fraudulent, holding MS KLJUČAROVCI liable for VAT.

- Legal Interpretation of Article 141: The referring court sought clarification on whether the simplification scheme for triangular transactions applies when goods are transported directly to a final customer rather than through the intermediary, as stated in Article 141(c) of the VAT Directive.

- General Court’s Ruling: The General Court ruled that the simplification measure can apply in a four-party chain without physical delivery to the third party; however, it also stated that tax authorities can deny this benefit if the intermediary knew or should have known about the VAT fraud involved in the transactions.

Source BTW Jurisprudentie

- The Court of First Instance determined that for the application of Article 141(c) of the VAT Directive, it is irrelevant whether MS Ključarovci, d.o.o. knew the goods were transported to the ANC Group instead of the three Danish companies, as long as the ANC Group is subject to VAT in Denmark.

- MS purchased goods from German companies, organized their transportation to Denmark, and applied a simplification measure for triangular transactions, transferring the VAT obligation to the Danish companies, despite the Slovenian tax authorities questioning the legitimacy of this arrangement due to the absence of those companies in Denmark.

- The court noted that MS could lose the simplification measure if it is proven that it was aware or should have been aware that its transactions were part of a VAT fraud scheme involving the supply chain, highlighting the importance of due diligence in VAT compliance.

Source Taxlive

See also

Source Fabian Barth

- Join the Linkedin Group on ECJ/CJEU/General Court VAT Cases, click HERE

- VATupdate.com – Your FREE source of information on ECJ VAT Cases

- Podcasts & briefing documents: VAT concepts explained through ECJ/CJEU cases on Spotify

Latest Posts in "European Union"

- VAT Applies to Retailer’s Tax-Free Refund Processing Fees: No Exemption, Fee Treated as Gross Price

- CJEU Confirms Triangulation VAT Relief Applies to Four-Party Chains, Even with Direct Customer Delivery

- Is User Data a Form of Payment? EU VAT Committee Explores Taxation of Digital Barter Transactions

- HMRC Reverses VAT Grouping Policy on EU Branches, Allowing UK Businesses to Reclaim Overpaid VAT

- CJEU Broadens VAT Exemption for Negotiation Services in Mortgage Intermediation Cases