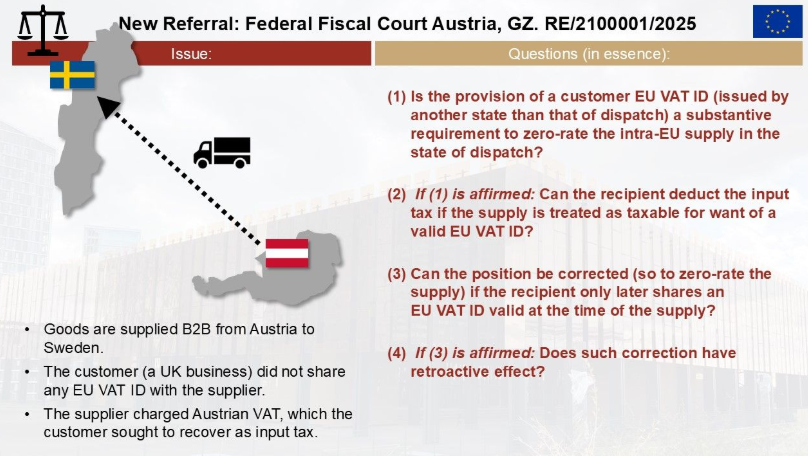

- An Austrian supplier charged VAT on a B2B supply to a UK business in Sweden (deliver to Sweden) because the customer didn’t provide an EU VAT ID, prompting the customer to seek input tax recovery.

- The Austrian Federal Fiscal Court has referred questions to the ECJ concerning whether a customer’s EU VAT ID is a substantive requirement for zero-rating intra-EU supplies, the possibility of input tax deduction without it, and if corrections can be made retroactively.

- The author suggests that the EU VAT ID is not a substantive requirement and that input tax deduction would likely be refused if the supply is treated as taxable due to the absence of a valid EU VAT ID.

Source Fabian Barth

See also

- Join the Linkedin Group on ECJ/CJEU/General Court VAT Cases, click HERE

- VATupdate.com – Your FREE source of information on ECJ VAT Cases

- Podcasts & briefing documents: VAT concepts explained through ECJ/CJEU cases on Spotify

Latest Posts in "Austria"

- Mandatory E-Invoicing for Austrian Federal Government Suppliers: Rules, Platforms, and Submission Methods

- Austria to Cut VAT on Staple Foods, Hygiene Products, and Contraceptives in 2026

- Subsidy Entitlement for VAT-Exempt Entrepreneurs Operating Care Homes Under Austrian Law

- VAT Exemption for High-Value Residential Rentals from 2026; Input VAT Deduction Disallowed

- Austria Introduces 4.9% Reduced VAT Rate for Essential Foods from July 2026