Understanding the Reemtsma-Claim and Its Implications for VAT Recovery

- A Reemtsma-claim allows taxpayers to seek recovery of unduly paid VAT from tax authorities when they cannot reclaim it from the supplier, particularly in cases of supplier insolvency or contractual time bars.

- The CJEU has expanded the scenarios for Reemtsma-claims to include situations where a supplier is time-barred from correcting their VAT obligations, thus reinforcing taxpayer rights.

- Importantly, the Reemtsma-claim is distinct from input tax deduction, with timing implications; input tax deductions are based on invoice receipt, while Reemtsma-claims arise only when recovering VAT from the supplier becomes impossible.

Source Fabian Barth

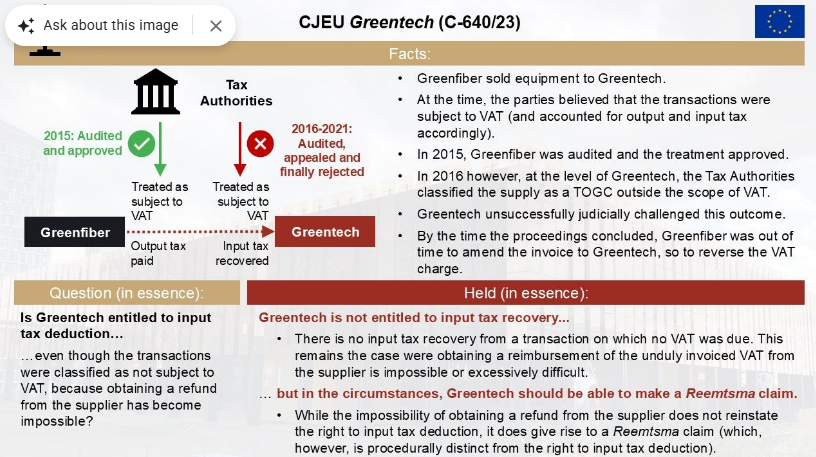

- The case involves a transaction between two Romanian taxpayers where the seller incorrectly charged VAT on asset sales. Initially, both companies treated the transaction as subject to VAT, leading the buyer to deduct input tax. However, audits revealed conflicting interpretations, with the seller’s audit suggesting VAT applicability and the buyer’s audit concluding it was not taxable.

- After lengthy legal proceedings spanning nine years, the Court determined that while the buyer cannot deduct input tax due to the transaction being non-VAT applicable, they still have the right to seek a refund directly from the tax authorities for the VAT paid to the seller. This ruling highlighted the complexities surrounding VAT corrections and the limitations on suppliers’ abilities to amend invoices.

- The Court’s reasoning emphasized that member states must define procedures for VAT corrections and that the buyer’s claim to the tax authorities does not equate to a right of deduction. This decision underscores the importance of understanding VAT obligations and rights, especially in cases of misapplied VAT, and serves as a crucial precedent for similar disputes in the future.

See also

Sources

- Join the Linkedin Group on ECJ/CJEU/General Court VAT Cases, click HERE

- VATupdate.com – Your FREE source of information on ECJ VAT Cases

Podcast by Piotr Chojnocki

Note that this post was (partially) written with the help of AI. It is always useful to review the original source material, and where needed to obtain (local) advice from a specialist.

Latest Posts in "European Union"

- Luxembourg VAT on Directors’ Fees: Impact of CJEU C-288/22 Ruling and District Court Decision

- Arcomet Case: CJEU Rules Transfer Pricing Adjustments Can Trigger VAT Obligations

- VAT Treatment of Transfer Pricing Adjustments: ECJ Ruling on Arcomet Towercranes

- VAT Treatment of Loyalty Points: Discounts vs Vouchers After ECJ Case

- EU Commission Publishes ViDA Implementation Strategy for Digital VAT System Modernization