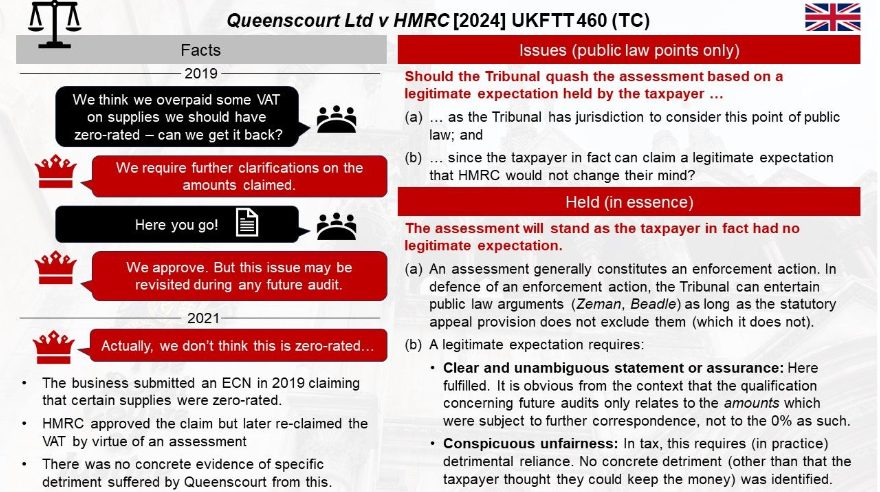

If tax authorities initially approve a tax refund claim but later change their decision, it may seem unfair. However, in legal proceedings based on a legitimate expectation, this alone is not enough. While there is occasional mention of the idea that “detrimental reliance” by the taxpayer is not strictly necessary, in practice it often is. This was evident in a court case and is generally the approach taken by the law. Businesses must be prepared for unexpected changes until the time limits for claims expire.

Source Fabian Barth

Latest Posts in "United Kingdom"

- Upper Tribunal: VAT Not Reduced on Pharma Payments by Boehringer Ingelheim to DHSC

- UT: Payments to DHSC by Medicine Manufacturer Not VAT Price Reductions; Rebate Mostly Denied

- Court Ruling Redefines VAT Status for Further Education Colleges: Key Impacts and Next Steps

- Tories Urge Three-Year VAT Cut on Energy Bills to Ease Cost of Living Crisis

- Upper Tribunal Rules VAT Not Reducible on BIL’s NHS Pharmaceutical Payments to DHSC