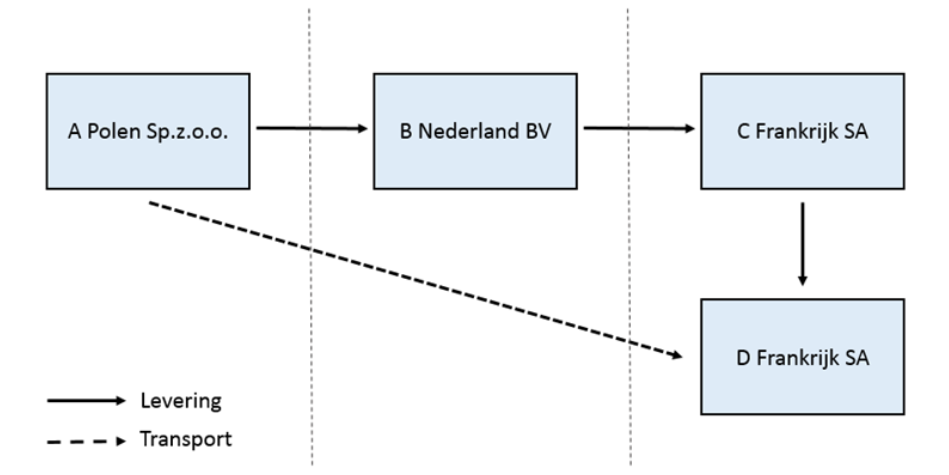

The Dutch tax authority has deemed that 4 party triangulation is permissible in certain cases. An example is given where a Dutch company purchases goods from a Polish supplier and arranges for the goods to be sent directly to the final customer in France. The French customer would self-account for the VAT due on the supply. It is noted that while this approach may be permitted in the Netherlands, other EU member states may have different rules.

Source Meridian

Latest Posts in "Netherlands"

- Reduced VAT Rate Not Applicable to Artistic Murals, Only to Residential Painting and Plastering

- Court Holds VAT Adjustment Dispute over City Hall Resolved by Settlement Agreement

- Dutch Court: Fiscal Representation Cannot Be Required for VAT Zero-Rate Where Mutual Assistance Exists

- Supreme Court Refers VAT Deduction Dispute on Mixed Costs in Financial Instruments to Hague Court

- No VAT Deduction Allowed for ICT Manager’s Mobile Phone Bundles, Court Rules