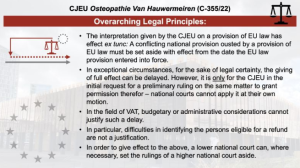

Where EU law rights are fiscally inconvenient, Member States may sometimes try to delay their implementation. In particular, they might attempt to refuse refunds of unduly charged VAT, to their own enrichment and the detriment of businesses. Gladly, the Court shows little mercy with such attempts. This is not generous, but plainly necessary: Had it been otherwise, Member States might impose taxes in breach of EU law, knowing full well that they can get away with it for a few years before being challenged.

Source Fabian Barth

See also

- Join the Linkedin Group on ECJ VAT Cases, click HERE

- VATupdate.com – Your FREE source of information on ECJ VAT Cases

Latest Posts in "European Union"

- Comments on ECJ C-436/24 (Lyko): Court Rules Loyalty Points Do Not Qualify as Vouchers

- EGC Customs T-589/24: No partial exemption from import duties in outward processing

- CJEU: OPR Import Duty Exemption Requires Export via Authorized Customs Office Only

- ECJ C-167/26 – ECJ will review EGC Case T-689/24 RX – VAT deduction and invoice timing

- Blog Part 5: Living with ViDA: Governing VAT and Finance in a Continuous Compliance Environment