Four main types of stakeholder are involved in the reform:

- Companies: suppliers, buyers or their representatives, with or without an internal or external (service provider) dematerialisation solution

- The public invoicing portal (PPF): the trusted public third party offering a minimum service and consolidating invoices and invoicing data for the tax authority

- Registered private platforms (PDPs): service providers offering dematerialisation services for invoices registered by the tax authority. Only registered private platforms can send e-invoices directly to their recipients and transmit data to the public invoicing portal.

- Dematerialising operators (ODs): operators offering invoice dematerialisation services, but which are not registered by the tax authority. These operators cannot send e-invoices directly to their recipients but must be connected either to the PPF or to a registered private platform (PDP).

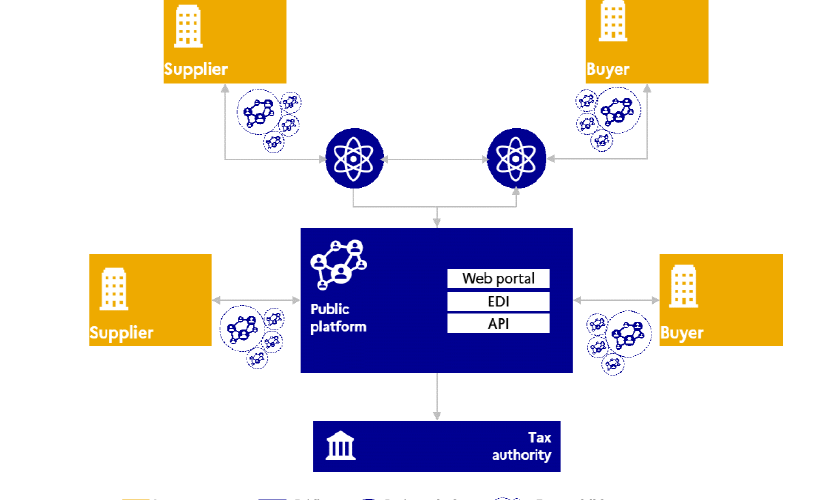

The ”Y scheme”

Article 289 bis of the French General Tax Code (CGI) provides that “the issue, transmission and receipt of electronic invoices shall be effected, at the choice of the parties, using the public invoicing portal referred to in Article L. 2192-5 of the Public Procurement Code or a registered private platform.

(…) Invoicing data issued by taxable entities using the public invoicing portal referred to in the second sub-paragraph of I shall be forwarded by the public invoicing portal to the tax authority. Invoicing data issued by taxable entities using another online platform shall be forwarded by the online platform operator to the public invoicing portal which shall forward it to the tax authority.”

To exchange invoices, companies may choose to go through a registered private platform of their choice which, once registered by the tax authority, can send the invoice directly to the recipient. In other cases, they may use the public invoicing portal, where they will be provided with free services allowing them to fulfil their obligations and exchange their invoices.

The scheme resulting from this article, and representing the relationship between the ecosystem stakeholders, is the so-called “Y”” scheme:

The mechanism adopted is based on reconciling:

- The freedom of each company to use the public invoicing portal or a registered private platform for issuing or receiving invoices;

- The requirement to report invoicing, transaction and payment data to the tax authority.

The “Y” scheme applies to both e-invoicing and e-reporting:

The e-invoicing feature allows the submission, transmission and tracking of domestic B2B and B2G invoices: the invoices may be sent directly to the public invoicing portal by companies (or their delegated representative). Registered private platforms will forward invoicing data submitted by their own clients to the public invoicing portal:

- When the public invoicing portal is the platform referenced in the directory for the receipt of invoices by a company (or its delegated representative); or

- When the public invoicing portal is a hub. This alternative does not exclude the first: as a hub, the public invoicing portal must systematically receive invoicing data for all invoices issued.

The e-reporting feature allows the public invoicing portal to process of data submitted directly on the PPF, for non-domestic B2B and BŹC transactions. All e-reporting data systematically goes through the public invoicing portal (direct submission by the company on the PPF or consolidation after submission via a registered private platform).

Source External specification file for electronic invoicing issued in English

See also

- Part 1 – Legal framework of E-Invoicing, E-Reporting & Transmission of payment data

- Part 2 – Timeline

Join the Linkedin Group on Global E-Invoicing/E-Reporting/SAF-T Developments, click HERE

Latest Posts in "France"

- France to Abolish Simplified VAT Regime from January 2027: Key Changes for Businesses

- France Publishes the New Customs Code: Ordinance n° 2026‑265 and Decree n° 2026‑266 Adopted

- France Clarifies VAT Rules for Dropshipping Without IOSS Scheme Participation

- French Court Clarifies VAT and Payroll Tax on Issuer Commissions and Incentives

- Tax Audits and Fiscalization: Comparing Germany, France, and Italy for Retailers and Professionals