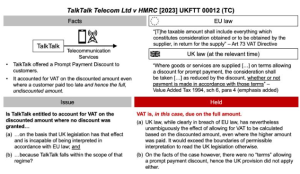

The judge found to be unambiguous the (now amended) provision allowing UK taxpayers to charge VAT on a discounted price even where the full price was received, and felt that it would exceed the boundaries of interpretation if it gave that provision an EU law-consistent meaning (which would in any case require VAT to be paid on the actual consideration received).

Source Fabian Barth

Latest Posts in "United Kingdom"

- Supreme Court Rules Against VAT Recovery on Hotel La Tour’s Fundraising Share Sale Costs

- UK Supreme Court Rules VAT on Share Sale Fees Not Recoverable for Business Funding

- UK Eases VAT Grouping Rules to Attract Foreign Investment and Simplify Cross-Border Compliance

- Tribunal Rules Bespoke Autobiography Books by Story Terrace Qualify for VAT Zero-Rating

- Full VAT Recovery Allowed on Product Photography Costs in Littlewoods v HMRC Tribunal Decision