?

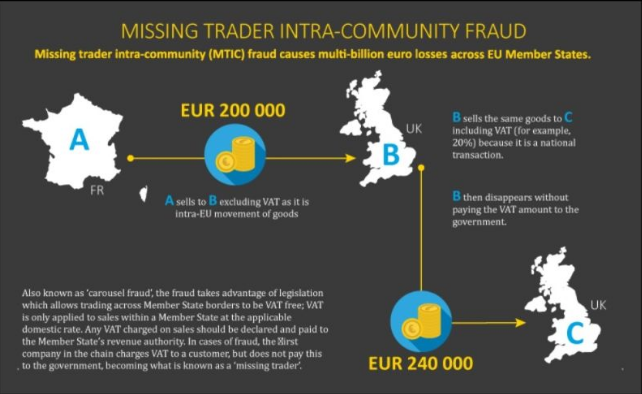

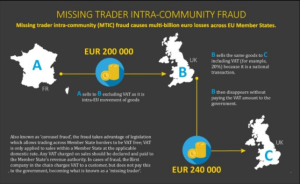

VAT fraud is the theft of value-added tax from a government by organised crime groups (OCG).

The most common scheme is Missing Trader Intra-Community (MTIC) fraud, where criminals take advantage of legislation that allows VAT free trading across EU Member States borders.

In the most complex cases, goods are imported and sold through linked companies before being exported again:

1️⃣ the first company charges VAT to a customer, but does not pay this to the government (missing trader);

2️⃣ the exporters claim and receive the reimbursement of VAT payments that never occurred;

3️⃣ additional “ ” can be interposed, so as to make it more difficult to identify the beneficiary of the fraud.

⚠️ The process can be repeated many times: this is why it is called .

Source Lorenzo Savastano

Latest Posts in "European Union"

- Comments on C-513/24 (Oblastní nemocnice Kolín) – Obligation for the presence of goods in hospital not decisive for VAT deduction

- EGC Customs T-296/25 (Lidikar) – Judgment – Use of Foreign Export Prices for EU Customs Valuation

- Comments on ECG T-689/24: Confirms Incompatibility of Polish Input VAT Deduction Rules with EU Law

- Comments on T-221/25: Implicit VAT taxation for non-EU travel services by agents is valid

- ECJ/General Court VAT Cases – Pending cases