This part of the Study covers ‘Digital Reporting Requirements’, that is any obligation for VAT taxable persons to periodically or continuously submit data in a digital way on all (most of) their transactions, including by means of mandatory e-invoicing, to the tax authority. As of September 2021, 12 EU Member States have introduced a Digital Reporting Requirement, with positive net impacts, as the additional VAT revenue exceeds the costs for setting up the system and complying with the requirements. However, the existing rules (or lack thereof) on Digital Reporting Requirements generate two main problems: (i) a fragmented regulatory framework, and (ii) an insufficient degree of fight against VAT fraud, for intra-EU transactions, as well as at a domestic level. The analysis of impacts of possible policy options shows that the best policy choice results from the introduction of an EU Digital Reporting Requirement. As for the type of requirement, the comparison suggests that an e-invoicing solution ranks first across the various scenarios.

Link to the Report

Source op.europa.eu

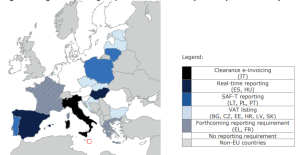

Just one extract: Digital Reporting Requirements in the EU (as of September 2021)

Latest Posts in "European Union"

- VAT Concepts Explained: Chain Transactions/Triangulation

- E-Invoicing in France, Germany, and Italy: Systems, Timelines, and Regulatory Models Compared

- EU Council and Parliament Agree on Major Customs Reform, Introducing Single Data Hub and New Authority

- EU Reaches Historic Agreement on Customs Union Reform, Modernising Rules for E-Commerce and Trade

- EU Customs Union Undergoes Major Reform for Smarter Data and Stronger Borders