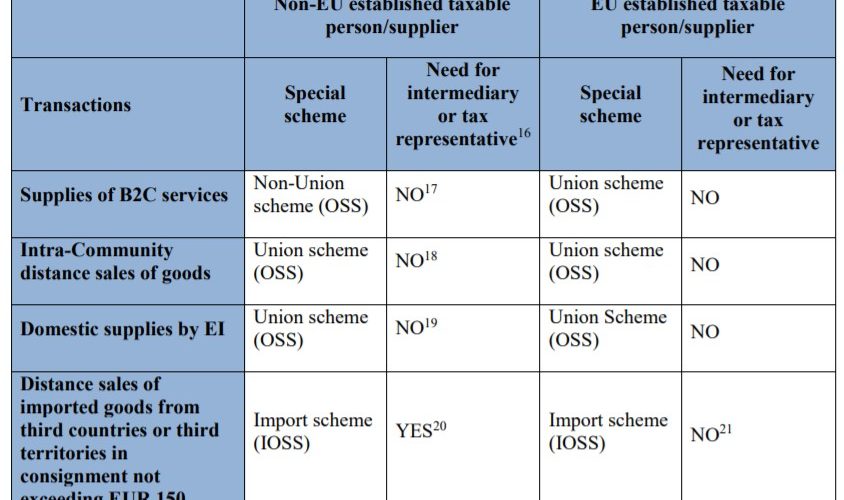

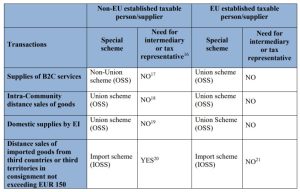

The new provisions modify the existing VAT special schemes15 laid down in the VAT Directive (non-Union scheme, Union scheme) and add a new one (import scheme). The below table provides an overview of the amendments that apply as from 1 July 2021.

- 17 Member States may not oblige non-EU suppliers to appoint a tax representative to use the non-Union scheme (Article 204 of the VAT Directive).

- 18 According to Article 204 of the VAT Directive, Member States may in this case require the taxable person to appoint a fiscal representative who will be the person liable to pay VAT.

- 19 According to Article 204 of the VAT Directive, Member States may in this case require the taxable person to appoint a fiscal representative who will be the person liable to pay VAT.

- 20 Except for a supplier established in a third country with which the EU has concluded an agreement on mutual assistance – see further details in chapter 4.

- 21 No obligation to appoint an intermediary to use the import scheme, but the taxable person is free to do so.

Latest Posts in "European Union"

- EU Pushes VAT Cuts to Accelerate Electrification

- Financial-Sector VAT, “Beyond ViDA” and Implementation: Inside the Joint GFV/VEG Minutes of 25 June 2026

- EU Annual Report on Taxation 2026: VAT Holds Firm as Consumption Taxes Cede Ground to Capital

- ECJ State Aid C-360/25 (X) – Judgment – National VAT Exemption Without Directive Basis Constitutes Unlawful State Aid

- Roadtrip through ECJ Cases – Focus on “Liability to pay VAT – VAT shall be payable by any person who enters the VAT on an invoice” (Art. 203)