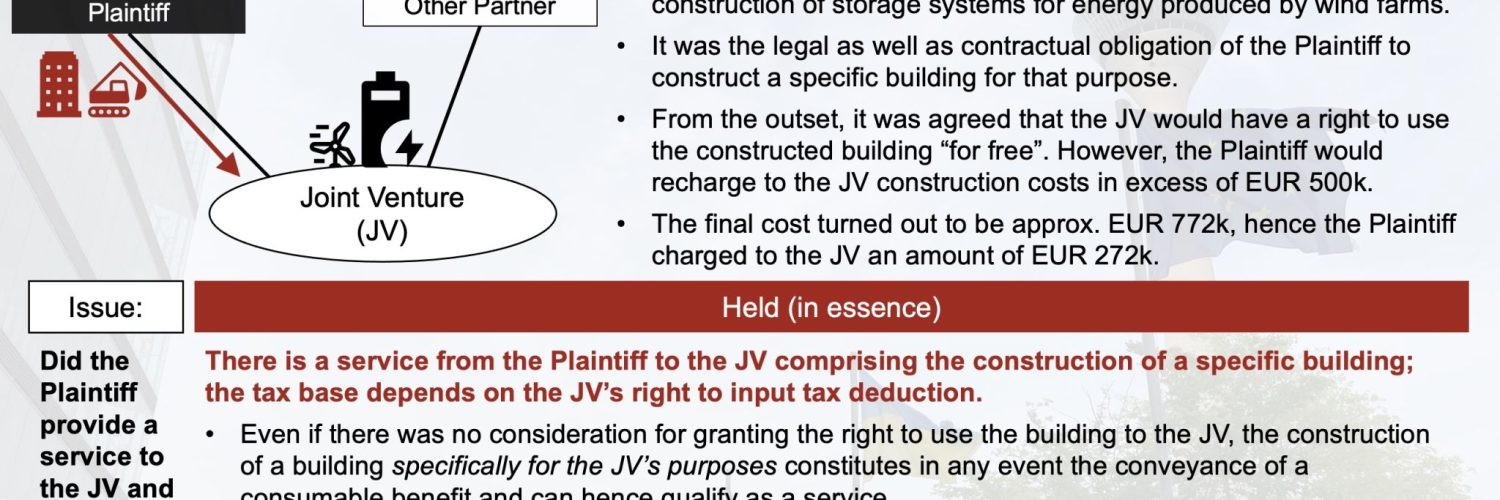

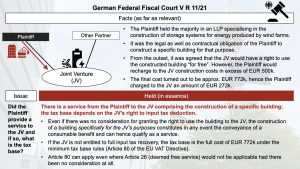

The case involved a taxpayer constructing a building for another party and allowing them to use it for free. The State Court initially ruled that there was no supply because the user did not receive anything in return for the construction costs. However, the Federal Court disagreed, stating that the construction of the building could be classified as a service and that the tax base could be elevated to EUR 772 due to some consideration being present. The interplay between Articles 26 and 80 of VAT law was noted as creating anomalous results, which the CJEU may need to review.

Source Fabian Barth

Latest Posts in "Germany"

- VAT Registration in Germany 2026: Requirements, Process, and Key Tax Numbers Explained

- VAT Returns in Germany 2026: Filing Deadlines, Frequencies, and ELSTER Submission Guide

- German VAT 2026: Rates, Rules, and Key Changes for E-commerce and Service Providers

- F-Gas and Ozone Regulation: Reporting Deadlines, ATLAS Requirements, and New Compliance Obligations for Companies

- Input VAT Deduction on Import VAT for EXW Deliveries: Munich Tax Court Decision of 09.12.2025